Table Of Content

- Benefits of making a larger down payment

- Check out today’s mortgage rates.

- Eden Prairie's Asia Mall opening a second north metro location

- Different Types of Mortgage Loans for Buyers and Refinancers

- Down Payment On Your Investment Property

- How much should you put down on a house for each loan type?

- Can you borrow from your retirement plan for a down payment?

By investing this amount (or more) on a purchase, borrowers can avoid the extra cost of private mortgage insurance (PMI). That’s because PMI is usually required whenever the loan-to-value ratio rises above 80%. So, let’s say this couple takes out a 30-year, fixed-rate mortgage at 7% for a $700,000 house, and makes a down payment of $140,000.

Benefits of making a larger down payment

This also might keep you from taking on more debt than you can handle. It is important to remember that a down payment only makes up one upfront payment during a home purchase, even though it is often the most substantial. There are also many other costs that may be involved, such as upfront points of the loan, insurance, lender's title insurance, inspection fee, appraisal fee, and a survey fee. A very rough estimate for the amount needed to cover closing costs is 3% of the purchase price, which is set as the default for the calculator.

Check out today’s mortgage rates.

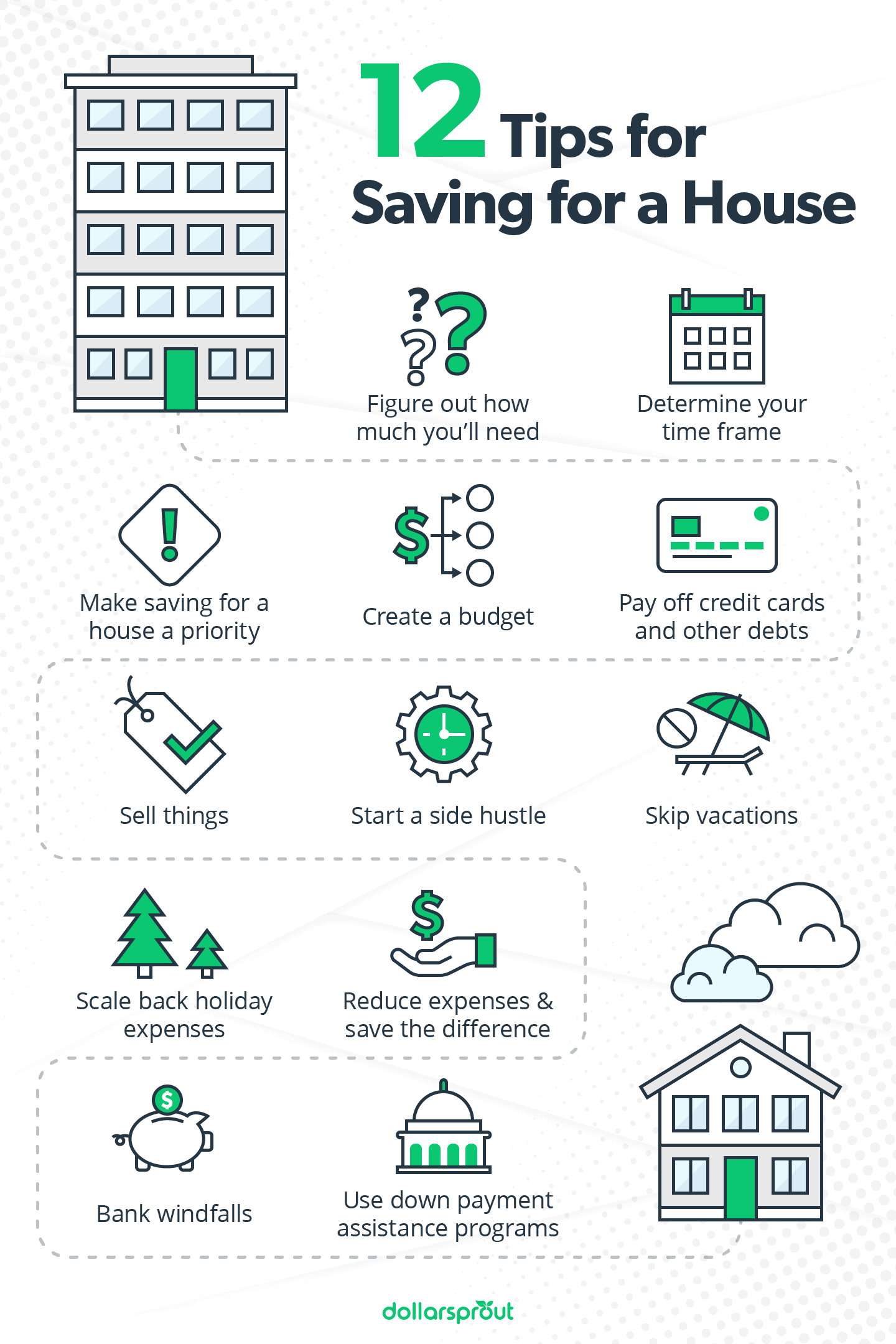

A big part of learning how to save up for a house is knowing how much you want to save. In addition to freeing up cash flow, eliminating these debts will lower your debt-to-income ratio and may increase your chances of getting approved for a loan. Learn what you need to know as you prepare to purchase your first place. With sky-high prices in LA, it might seem daunting to save for a home.

Eden Prairie's Asia Mall opening a second north metro location

Most significantly, it can reduce the cost you pay to borrow money over the life of the loan. Reducing the amount you need to borrow, even by a little bit, will lower the amount you pay in interest over time, and it can lower your monthly payments as well. The down payment is the portion of the home’s purchase price that you pay upfront and is not financed through a mortgage. The down payment directly reduces the amount of money you need to borrow for the home purchase.

Different Types of Mortgage Loans for Buyers and Refinancers

Keep in mind, too, that to avoid PMI, you’ll need to put down at least 20 percent. If you can’t afford that high of a down payment, though, know you won’t pay PMI forever. Once you reach 20 percent equity in your home, you can request that your lender remove PMI from your bill. For a conventional loan, you’ll need to put at least 20% down to avoid PMI. If you put down less than this, you’ll have to pay PMI until your loan has reached 80% of the original home value or you’ve reached the halfway point of your repayment term.

Down Payment On Your Investment Property

Tim Lucas spent 11 years in the mortgage industry and now leverages that real-world knowledge to give consumers reliable, actionable advice. Tim has been featured in national publications such as Time, U.S. News, MSN, The Mortgage Reports, and more. The three calculations below offer different ways to help calculate an estimated down payment.

How Much Do You Need for a Down Payment on a Home in Colorado? - K99

How Much Do You Need for a Down Payment on a Home in Colorado?.

Posted: Mon, 04 Mar 2024 08:00:00 GMT [source]

If your loan requires other types of insurance like private mortgage insurance (PMI) or homeowner's association dues (HOA), these premiums may also be included in your total mortgage payment. Offer valid on primary residence, conventional loan products only. Cost of mortgage insurance premium passed through to client effective January 2, 2024. Offer valid only for home buyers when qualifying income is less than or equal to 80% area median income based on county where property is located. Not available with any other discounts or promotions and cannot be retroactively applied to previously closed loans or loans that have a locked rate.

Take your smart money habits to the next level

Hit your goals with these creative ways to save for a downpayment. As such, Californians thinking of purchasing property should create a budget and begin saving for a down payment well in advance of deciding to buy a home. To help point aspiring homeowners in the right direction, the team at Prevu Real Estate gathered the answers to the key topics buyers ask about when saving for a down payment.

Can you borrow from your retirement plan for a down payment?

So, using the figure of $150,000, that would equal a maximum housing expense of $3,500 per month ($150,000/12 x 28%). Get expert tips, strategies, news and everything else you need to maximize your money, right to your inbox. If you do make a smaller down payment, keep in mind you'll start out with less equity in your home. In general, the younger a buyer is, the more likely they are to make a smaller down payment. Victoria Araj is a Section Editor for Rocket Mortgage and held roles in mortgage banking, public relations and more in her 15+ years with the company.

With a smaller down payment, you’ll pay this expense for the life of the loan. You could also consider a rent-to-own arrangement, where you rent a home with the option to buy it later. During the rental period, a portion of your payments will cover the rent while the rest will be put toward a down payment on the house.

Although placing down payment savings in higher risk investments such as stocks or bonds can be more profitable, it is also riskier. For more information about or to do calculations involving savings, please visit the Savings Calculator. For more information about or to do calculations involving CDs, please visit the CD Calculator. Down payment size is also important to lenders; generally, lenders prefer larger down payments. This is because big down payments lower risk by protecting them against the various factors that might reduce the value of the purchased home. In addition, borrowers risk losing their down payment if they can't make payments on a home and end up in foreclosure.

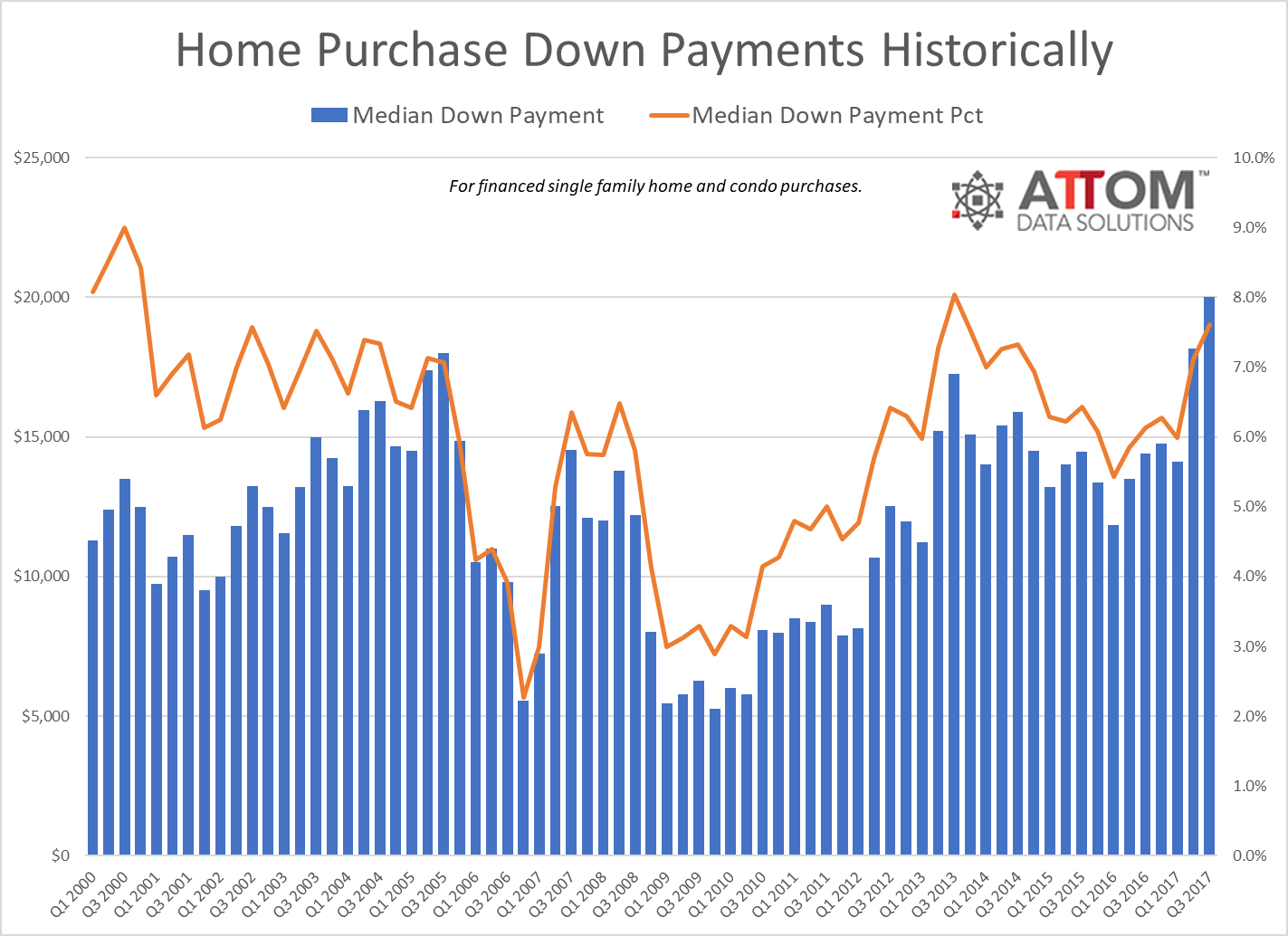

Many homebuyers, especially first-time buyers, don’t have a 20% down payment. In February 2023, the median existing-home price was $363,000, so an upfront payment of 20% is a hefty $72,600. Per rules set by government-sponsored entities Fannie Mae and Freddie Mac, the minimum down payment is 3% for conventional home loans.

This means Los Angeles residents need an annual income of $249,471 to comfortably afford a median home, but only make $87,743 – a staggering $161,728 less than needed. Some areas have a higher cost of living and higher property taxes. Another rule of thumb often applied when buying a home is to not spend more than three times your annual income on a home. Not every lender uses the same standards for mortgage qualification, whether you’re buying a $70,000 home, a $700,000 home or a $7 million home. You should be able to find a home with a median sale price of $700,000 or less in most metro areas in the U.S.

Whatever you have leftover after paying essentials like food, clothing, and utilities is how much you can afford to spend on housing. Applying for down payment assistance can add weeks or months to your home buying timeline, but for more information, the U.S. Department of Housing and Urban Development (HUD) keeps a list of programs listed by state, county, and city. So, if you earn $100K, your housing costs should be less than $28,000, $2,333 a month, and your debt and housing costs should not exceed $36,000, or $3,000 a month. Using the current statewide median home price of $833,910, a down payment of 20% would come to around $166,782.

Second homes typically start at 10 percent, and investment properties can require as much as 15 to 25 percent. That said, the amount you need for a down payment on a house can depend on your creditworthiness and financial situation. Consult with your loan officer to get a better idea of what requirements apply to you. Saving up for a traditional 20% down payment is time-consuming and challenging for home buyers with limited finances.

No comments:

Post a Comment